Gaspard LEZIN

Agentic Payment: What It Is and How It Works in 2026

Learn what an agentic payment is and how autonomous AI agents will change commerce. A guide to the tech, business impact, and USDC settlement.

You probably already have workflows that feel half-automated. A support bot upgrades a customer plan after usage spikes. A community tool checks whether a member has paid before granting access. A procurement assistant finds a dataset, calls an API, and gets right to the point where money has to move.

That last step is where most systems still break.

Businesses can automate discovery, orchestration, and fulfillment, but payment still assumes a human is present to click, approve, and reconcile. Agentic payment changes that. It treats payment as part of the software workflow itself, not as a handoff to a person or a banking process built for office hours.

Table of Contents

A simple definition

How it differs from normal automation

The basic HTTP 402 flow

Why this matters for product teams

Why legacy rails struggle

Traditional Payments vs Agentic Payments on Stablecoin Rails

Usage-based SaaS without manual billing logic

Paid communities that manage access automatically

On-demand machine-to-machine services

What the settlement layer needs to do

The practical building blocks

Where to start inside your business

What good preparation looks like

What Is an Agentic Payment

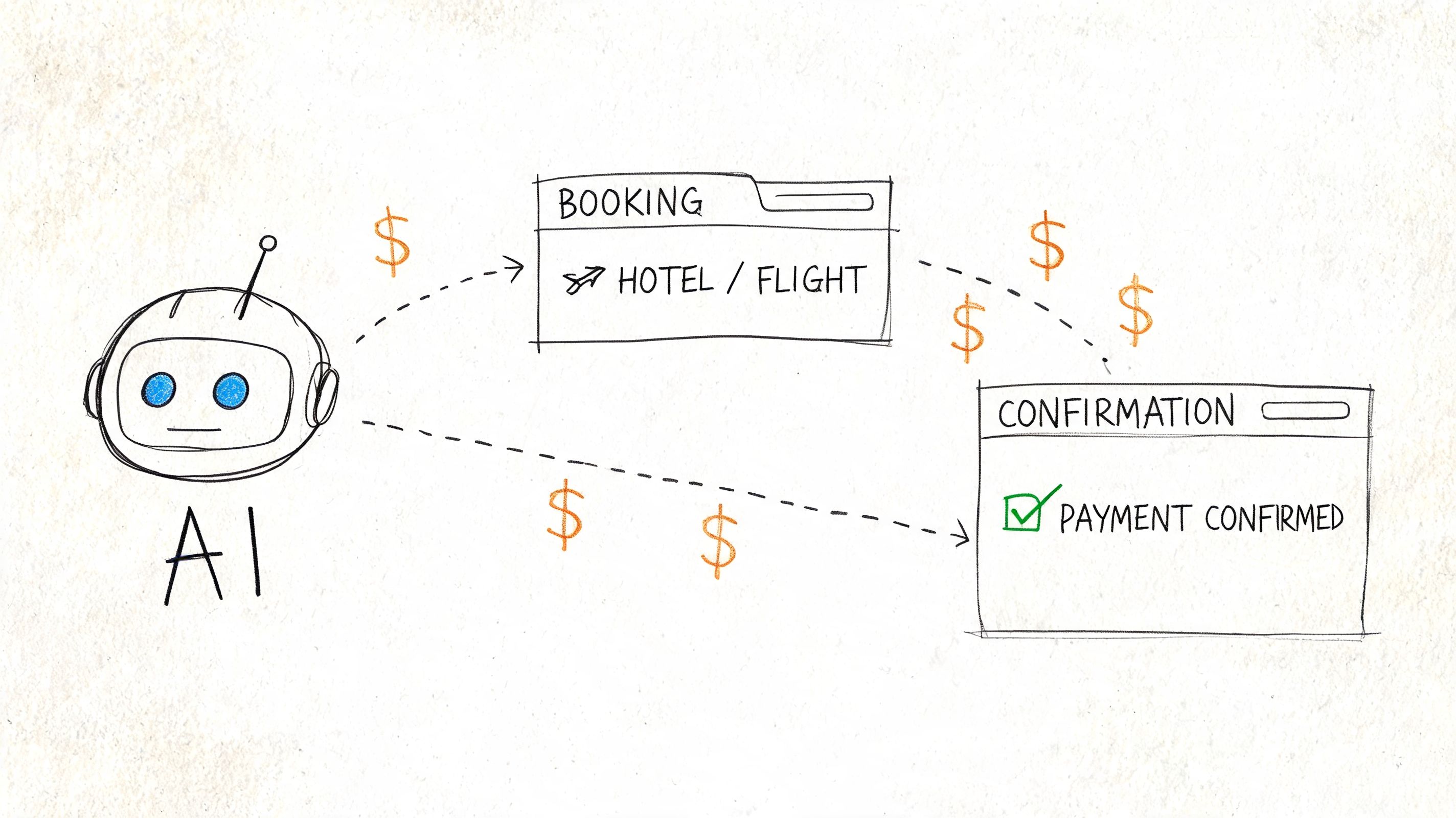

An easy way to understand agentic payment is to start with a familiar workflow. You ask an AI assistant to book a business trip within a policy limit, buy the best flight that fits your schedule, and reserve a hotel near the meeting venue. The assistant searches, compares, selects, and pays, without waiting for you to approve each screen.

That final transaction is the key. An agentic payment is a payment initiated and completed by a software agent based on delegated instructions, rules, or permissions, without a human manually clicking “pay” at the moment of purchase. The human still defines the objective and the boundaries. The software handles execution.

A simple definition

Digital commerce is shifting from people driving every step to software handling more of the workflow. The broader agentic economy is projected to reach a global market size of $3 trillion to $5 trillion by 2030 according to Nevermined’s analysis of AI agent payment statistics. You don’t need to agree with every forecast to see the underlying direction. More software is being asked to act, not just recommend.

If you're tracking the future of no-code AI agents, you can already see why payment becomes the bottleneck. Building an agent is getting easier. Giving that agent a safe way to transact is harder.

Practical rule: If your workflow still pauses for a manual checkout step, it isn't fully agentic yet.

How it differs from normal automation

Readers often confuse agentic payment with recurring billing or a stored card on file. They’re related, but they’re not the same thing.

A recurring subscription follows a preset schedule. An agentic payment makes a context-based decision within a permission scope. It might buy extra compute because usage crossed a threshold, renew a SaaS seat because a team still needs access, or purchase a one-time data service because the current task requires it.

It also differs from a normal payment service provider flow where a user types card details into checkout and confirms the transaction. If you want a grounding in that older model, this overview of what a PSP is is useful because it shows exactly what agentic systems are trying to move beyond.

The deeper question isn't whether software can decide to buy. It can. The harder question is what payment infrastructure can support millions of software-driven transactions without adding human friction back into the loop.

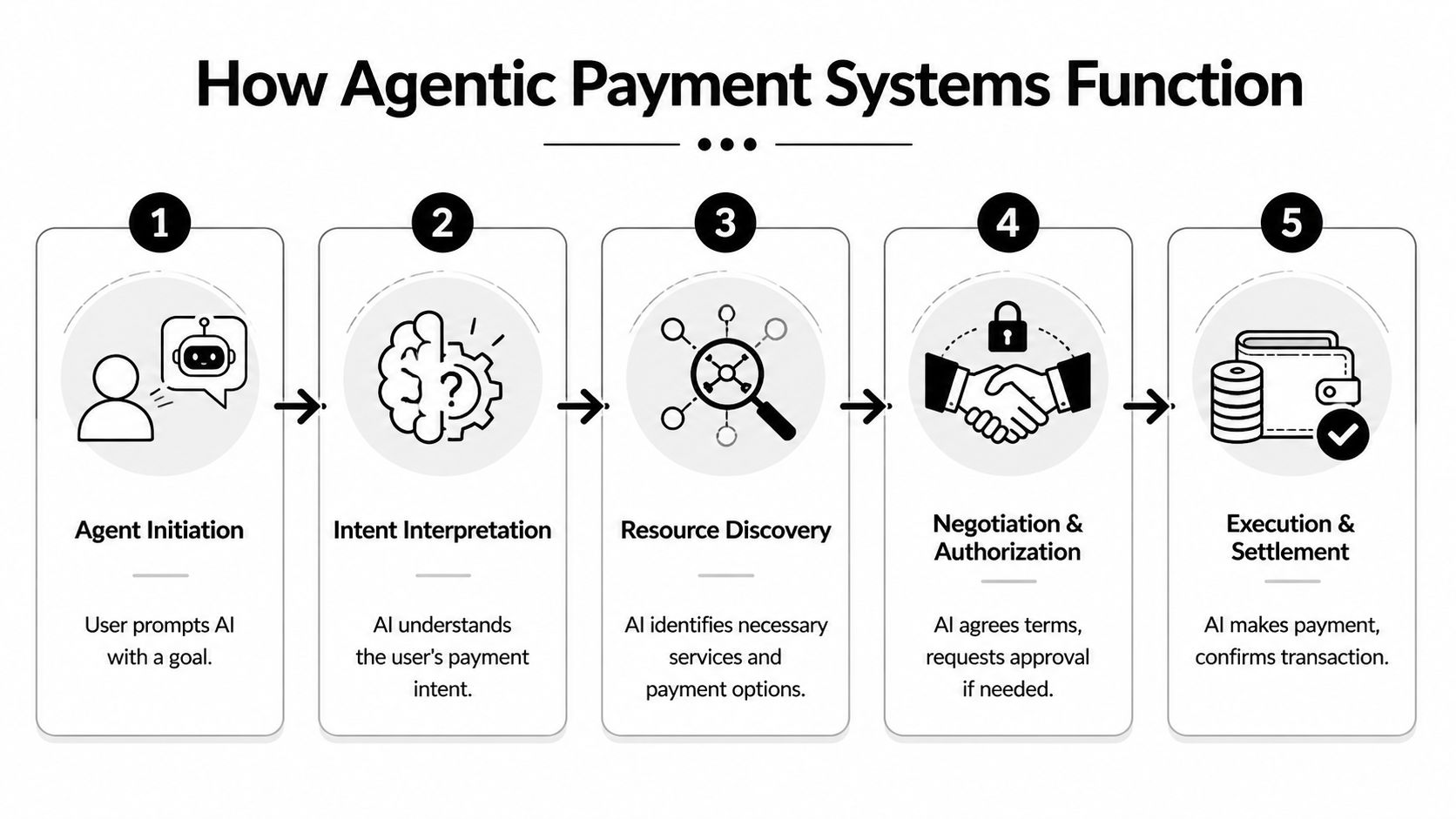

How Agentic Payment Systems Function

The term “agentic payment” often leads to the initial assumption that it requires a mysterious AI-only payment stack. In practice, the logic is more grounded than that. It’s a machine-to-machine request, a payment challenge, a proof of payment, and then access to the resource.

The basic HTTP 402 flow

A useful technical anchor is the HTTP 402 Payment Required pattern. According to Cloudflare’s agentic payments documentation, the flow works like this:

The client requests a resource.

An agent asks for access to a tool, API, dataset, or service.The server returns a payment challenge.

Instead of just denying access, the server responds with HTTP 402 and says payment is required.The client pays and retries.

The agent fulfills the payment request and sends the request again with payment credentials.The server verifies and returns the resource.

Once payment is confirmed, the service responds with the requested output and can include a receipt.

That flow sounds simple, but it changes how commerce can work online. Payment becomes part of the protocol itself. The service doesn’t need a long onboarding flow first. It can expose a paid action directly to another machine.

Why this matters for product teams

For technical business owners, the practical shift is this: you can design products where value is sold in small, programmatic increments. A model call, a premium feature, a content access, or a one-time action can all become payable events.

That has implications for product design:

Access control gets tighter: You can gate usage at the exact moment value is delivered.

Billing gets more granular: Teams can charge for actions, not just broad monthly plans.

Automation gets cleaner: The same software workflow that discovers a service can also pay for it.

A second area where people get confused is identification. How does a merchant know whether the agent is acting with real authority, rather than impersonating a user or running outside policy?

Google’s work on the transaction identification API is helpful context here because it shows why agent-aware identity matters in machine commerce. The payment system needs a way to understand not just who is paying, but whether an agent was authorized to act.

Payment isn't the hard part by itself. The hard part is tying payment, identity, and permission together in a way machines can use safely.

The result is a new product pattern. A user gives an agent a bounded objective. The agent discovers services, receives a payment request, proves authority, pays, and continues the task. No checkout page is required in the middle unless a policy says one is required.

For businesses, that opens a practical design question. If another piece of software wanted to buy from you right now, could your current payment stack support that cleanly?

For teams exploring global acceptance and programmable checkout, a practical reference point is this guide to a global payment API, because the integration problem is rarely just “can I take a payment?” It’s “can I take a payment in a way software can reliably trigger and reconcile?”

The Business Case for a New Payment Layer

The commercial case for agentic payment doesn't start with AI hype. It starts with the failure modes of traditional payment rails.

Human-centered systems assume someone can pause, review, approve, and wait. Machines don't work that way. If an agent needs to buy an API call, renew access, or settle a service request across borders, a multi-step bank process introduces delay at the exact moment the software is trying to complete a task.

Why legacy rails struggle

Three constraints show up quickly.

First, settlement is often slower than the software workflow itself. The agent can discover and decide in seconds, but the money movement may still follow delayed payout cycles.

Second, cross-border flows add friction. Currency conversion, reconciliation gaps, and banking intermediaries weren't designed for high-frequency, software-driven transactions.

Third, authorization models are built for humans. Card forms, redirects, and manual review all make sense when a person is buying a product. They create unnecessary friction when software is acting inside a bounded mandate.

This is why stablecoins keep coming up in serious discussions of agentic payment infrastructure. According to Nevermined’s analysis of the agentic economy and transaction volume, stablecoin transaction volumes hit $46 trillion annually by 2025, with 83% year-over-year growth. In the same source, these rails are positioned as foundational to high-velocity, borderless machine transactions that legacy systems struggle to support.

The point isn't that every business suddenly needs to think like a crypto-native company. The point is simpler. Software-driven commerce needs a settlement asset that moves at internet speed and works globally. USDC is one of the clearest fits for that role because it supports programmable, direct settlement without rebuilding the customer-facing checkout experience from scratch.

Traditional Payments vs Agentic Payments on Stablecoin Rails

Attribute | Traditional Payment Rails | Agentic Payments with USDC |

|---|---|---|

Primary design assumption | Human present at checkout | Software can execute within permission rules |

Settlement model | Often delayed and bank-dependent | Fast, programmable digital settlement |

Cross-border handling | Often includes FX friction and intermediaries | Better suited to global internet-native flows |

Best billing unit | Orders, invoices, recurring cycles | Fine-grained usage, events, and micro-transactions |

Machine-to-machine fit | Awkward, because it expects forms and manual review | Natural, because payment can be embedded in workflows |

Reconciliation | Often split across processors, banks, and ledgers | Cleaner when settlement is unified in a digital asset |

Customer experience | Familiar for human buyers | Can stay familiar for buyers while modernizing merchant settlement |

A lot of businesses will keep the front end users already understand. Card checkout isn't going away. The major shift is in the settlement layer behind it.

Strategic takeaway: The winning stack may look traditional to the buyer and programmable to the business.

That’s the part many articles skip. They focus on autonomous shopping and ignore the infrastructure question underneath. But if the settlement layer can't support software-speed transactions, the agentic workflow remains a demo, not a business model.

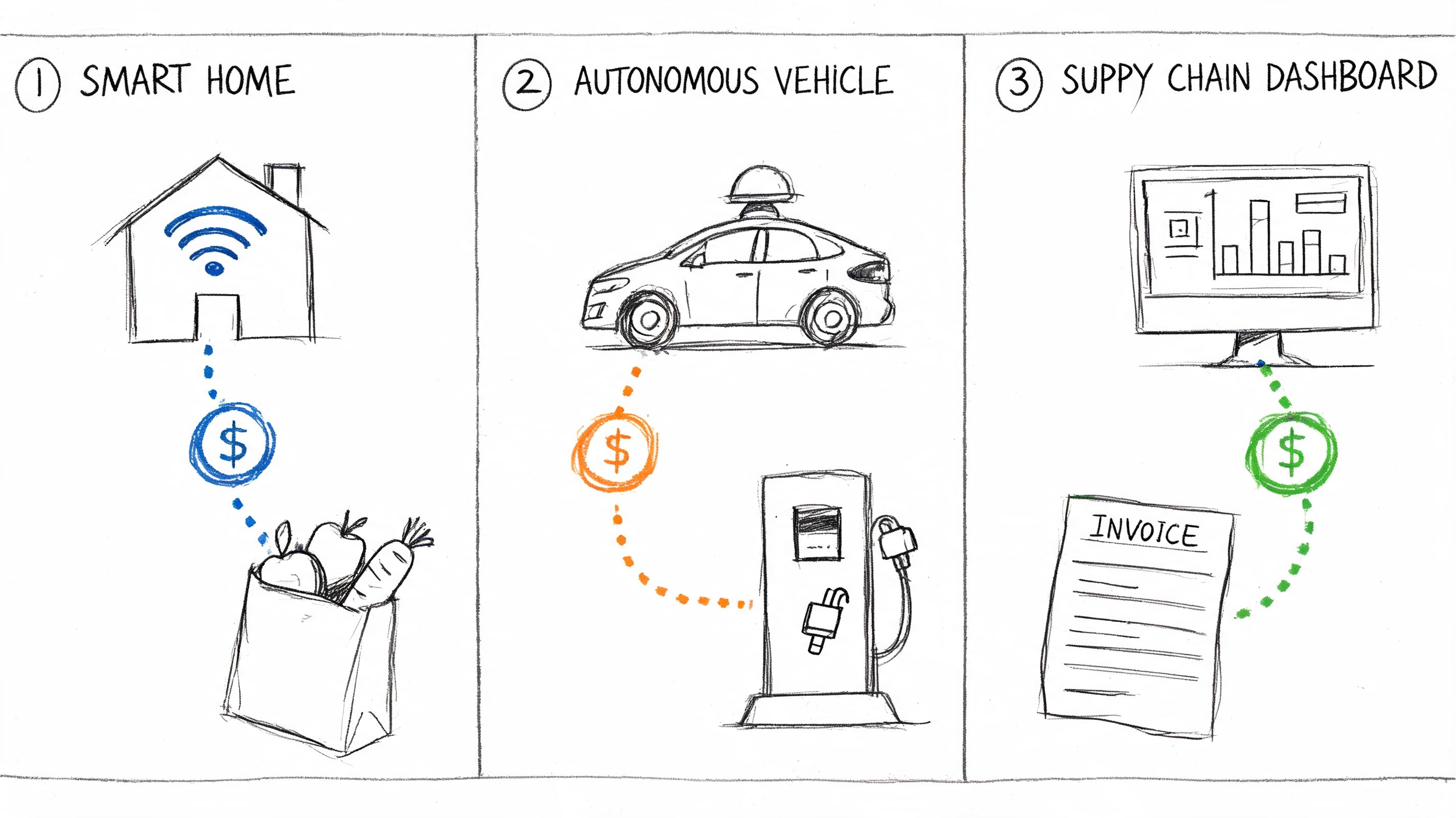

Agentic Payments in Action

The easiest way to see the value is to stop talking about theory and look at workflows businesses already run.

Usage-based SaaS without manual billing logic

A SaaS company sells data enrichment to developers. Customers start on a normal monthly plan, but usage varies a lot. Some tenants need extra capacity for a launch week, then drop back down. Others hit paid thresholds unpredictably because their own apps are growing.

In a traditional model, the company either overbuilds billing logic or forces users into blunt pricing tiers. An agentic payment approach creates another option. The customer delegates spending rules to a software agent, and the agent can approve a context-specific purchase when usage requires it.

This is where mandate-based authorization becomes important. According to the AP2 specification, Google’s Agent Payments Protocol introduces the PaymentMandate, a digitally signed, verifiable credential that binds agent permissions to specific transaction contexts such as permitted actions, spending limits, and use cases. In plain language, that means the system can tell the difference between “the agent is acting within delegated rules” and “something looks compromised.”

The business benefit is straightforward. The SaaS company can monetize real usage without forcing the buyer through a fresh approval loop every time a threshold changes.

Paid communities that manage access automatically

Now take a creator or operator running a paid Discord or Telegram community. The painful part usually isn't collecting money once. It's dealing with the full lifecycle afterward: checking who paid, updating roles, removing access after failed renewals, and handling refunds without breaking trust.

An agentic payment pattern lets software handle those steps as a coordinated flow. A customer pays. The system confirms settlement. A bot updates access. If the subscription changes state later, the same system updates permissions again.

For this type of workflow, video is often easier than description alone:

The important part isn't whether the buyer thinks in terms of AI. Most won't. They just experience a cleaner product. Pay, get access, keep access while active, lose access when the subscription ends, all without manual admin work.

If your product includes payment plus entitlement, the real opportunity is automating both at the same time.

On-demand machine-to-machine services

A third pattern is direct machine commerce. One agent needs a service from another system right now. It might need a premium dataset, a translation pass, an image generation step, or a one-time compliance check.

In old architectures, that often requires contracts, account setup, API keys, invoicing, and later reconciliation. In an agentic flow, the service can expose a priced action directly. The calling agent decides whether the action fits its mandate, pays for that one event, and continues the task.

This creates new product possibilities:

Pay-per-action tools instead of only monthly plans

Just-in-time service procurement without sales-led onboarding

Smaller monetizable units for APIs, agents, and digital services

These use cases matter because they don't require a science-fiction future. They require practical coordination among permissions, payment triggers, and settlement. Once those pieces work together, agentic payment stops sounding abstract and starts looking like a new revenue design pattern.

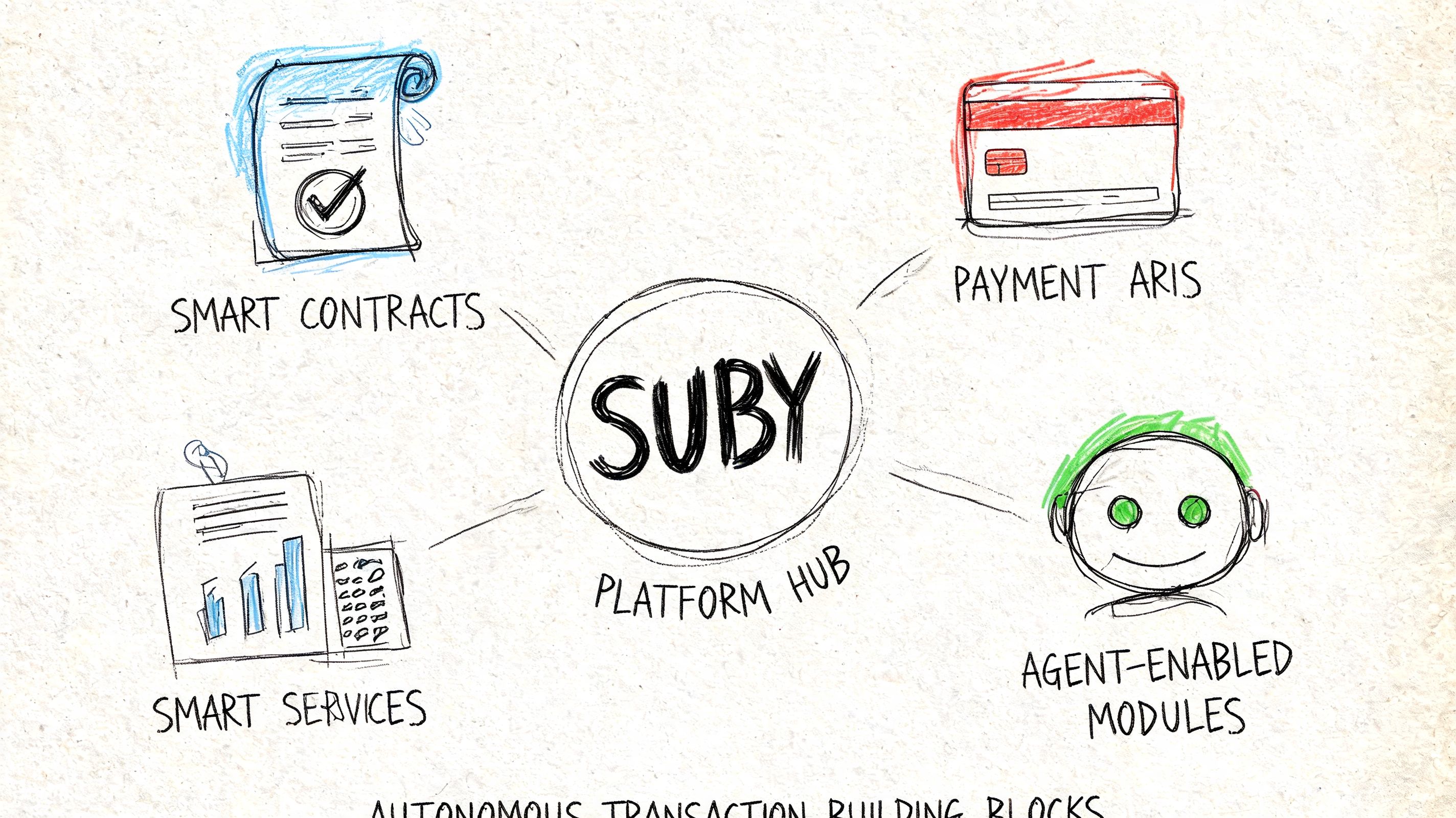

How to Enable Agentic Payments with Suby

Most writing on agentic payment spends its energy on the buying moment. The harder operational question is what happens after authorization. How does money settle, how does the business receive it, and how does the workflow stay reliable across borders?

What the settlement layer needs to do

That settlement problem is why stablecoin-native infrastructure matters. As noted in this PaymentsJournal discussion of agentic payments and global financial flow, a widely overlooked issue is the infrastructure required for stablecoin rails like USDC. Traditional rails introduce delays and FX fees, while systems built for instant USDC settlement remove banking intermediaries from the payout path.

For an online business, the practical requirement is simple:

Accept familiar payment methods for customers

Settle predictably in USDC for the business

Expose APIs and webhooks so software can react to payment events

Handle recurring and one-time flows without manual reconciliation

That combination is what makes agentic behavior commercially usable instead of technically interesting.

The practical building blocks

Suby fits this model because it provides an API that lets businesses accept payments by card or crypto, while the business receives USDC. That’s the core idea to keep in view. Users pay with cards, businesses receive USDC.

The same model is useful whether the workflow is human-led or software-triggered. An agent can generate or trigger a paylink, listen for a webhook, confirm payment state, and then kick off fulfillment. The business doesn't need to redesign everything around a wallet-native customer experience just to modernize settlement.

For community products, the pattern is even more direct. Suby also offers native integrations with Discord and Telegram for subscriptions, paid access, and online communities. That matters because agentic workflows often involve entitlement changes after payment, not just payment acceptance itself.

A practical reference for implementation is this guide to payment gateway API integration, especially if you're mapping the difference between a normal checkout integration and a software-driven payment workflow.

The most important design choice is architectural, not cosmetic. Keep the customer side flexible. Keep the settlement side deterministic. If users want to pay with card, let them. If your business wants unified USDC settlement, build around that.

Preparing Your Business for the Agentic Economy

Most businesses don't need to launch a fully autonomous buyer tomorrow. They do need to identify where payment still blocks software from completing work.

Where to start inside your business

Start with tasks that already have clear rules:

Usage expansions: A service crosses a threshold and needs more capacity.

Subscription continuity: Access should renew, pause, or end based on payment state.

Digital fulfillment: A system should deliver an output only after payment is confirmed.

Community access: Roles and permissions should track membership status automatically.

These are good candidates because they already involve logic, state changes, and repetitive payment decisions.

A second priority is governance. Agentic payment isn't just about speed. It requires permissioning, refund handling, and clean lifecycle control. That point is often underexplained in the market, but it matters more than the demo. As discussed in this SRM analysis of agentic payments as a competitive issue, liability and permissioning frameworks are critical, and Suby addresses this with features such as zero-fee refunds and unified access management through its API.

What good preparation looks like

Good preparation usually looks less glamorous than people expect.

It means defining what an agent is allowed to buy. It means setting spending boundaries, approval conditions, and fallback rules. It means choosing infrastructure that can support card acceptance on the front end and predictable USDC settlement on the back end.

If you're watching how automation is reshaping financial operations more broadly, Refact’s piece on RPA in banks is a useful adjacent read. The core lesson carries over. Automation only works well when process design, controls, and execution rails are aligned.

Final perspective: Agentic payment isn't a separate trend from modern payments. It's what happens when software automation reaches the money layer.

The near-term winners will be businesses that make one practical shift. They’ll stop treating payment as a disconnected checkout event and start treating it as programmable infrastructure. When customers can pay with cards, and the business can receive USDC with clear, software-friendly settlement, many of the hard parts become much easier to automate.

Suby is a payment gateway and payment processor. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. Its API and webhooks let software trigger and reconcile payments programmatically, so it works as the settlement layer for agentic payment flows that need to move at internet speed rather than wait on human checkout.