Gaspard LEZIN

How to Accept Credit Card Payments A Global Merchant Guide

Learn how to accept credit card payments with this practical guide. Explore payment processors, compliance, fees, and modern settlement options like USDC.

If you want to accept credit card payments, you traditionally needed a payment processor and a merchant account to manage all the messy details of authorization, clearing, and settlement. Thankfully, modern platforms have bundled all of this, letting you get started almost instantly with simple tools like payment links, embedded checkouts, or APIs.

The real trick is picking the right solution that actually fits how you do business and where your customers are.

Why Credit Cards Are A Must-Have For Global Growth

In today's market, not accepting credit cards is basically telling a huge chunk of your potential customers to go away. E-commerce is built on card payments, and people everywhere expect that convenience and security, though offering alternative payment methods alongside cards can widen the audience you reach. If you don't offer it, you're just creating friction that costs you sales and kills your growth, especially if you're trying to sell internationally.

Imagine you’re a SaaS company in Europe with a great product you want to sell in North America and Asia. Without a solid way to handle international credit cards, you’re up against some serious, and completely avoidable, headaches:

Sky-High Cart Abandonment: A clunky or unfamiliar checkout makes people nervous. They’ll just leave before they ever hit "pay."

Frustrating Payment Declines: Traditional banks are notorious for flagging cross-border transactions as risky, which means perfectly good customers get their cards declined for no reason.

Profit-Eating Currency Fees: You end up losing a surprising amount of money to forced currency conversions and terrible exchange rates. It's a silent killer for your profit margins.

Painfully Slow Payouts: Waiting days—or even weeks—for your money to show up from traditional bank settlements is a nightmare for cash flow.

This isn't some rare horror story; it's the default experience for too many businesses. The good news is that understanding how the system works is the first step to fixing it for good.

A Quick Look Under The Hood

Every single time a credit card is swiped or a number is typed online, a few key players are working behind the scenes. Modern payment platforms hide most of this complexity, but it’s still helpful to know who’s doing what.

Payment Gateway: Think of this as the digital version of a credit card terminal. It’s the secure front door that grabs the customer's payment info and encrypts it before sending it on.

Payment Processor: This is the middleman doing all the legwork. It routes the transaction details back and forth between your business, the customer's bank (the issuing bank), and your bank (the acquiring bank).

Merchant Account: This isn't your regular business bank account. It's a special holding account where the funds from card payments sit before they're officially transferred to you.

The sheer scale of this is mind-boggling. The global credit card payments market was valued at USD 622.76 billion in 2024 and is expected to more than double to a staggering USD 1,433.49 billion by 2034. This kind of explosive growth, tracked in Technavio's market analysis, shows that having a killer payment setup isn't just a nice-to-have anymore—it’s critical for survival.

Modern payment solutions let you sidestep the old, clunky hurdles of cross-border sales. The entire game is to make it dead simple for customers to give you their money, no matter what country they’re in.

Newer solutions package all these components into one platform, which simplifies everything. They take care of the security, compliance, and multi-currency chaos so you can focus on building your business, which is exactly what makes modern international business payments far easier to run than they used to be. For any company selling globally, getting the details of processing international payments right is key to boosting revenue and keeping customers happy. Let's walk through exactly how to put these modern tools to work.

Choosing The Right Way to Accept Payments

Your first big decision is figuring out how you’re going to take someone’s money. This choice goes way beyond just the transaction itself; it shapes your customer's experience and determines how easily your business can grow. What works for a freelancer invoicing a single client is completely different from what a SaaS platform needs to manage thousands of subscribers.

The right method really boils down to your business model, how comfortable you are with technology, and how much control you want over the checkout process. Let’s walk through the three main approaches to see which one makes the most sense for you.

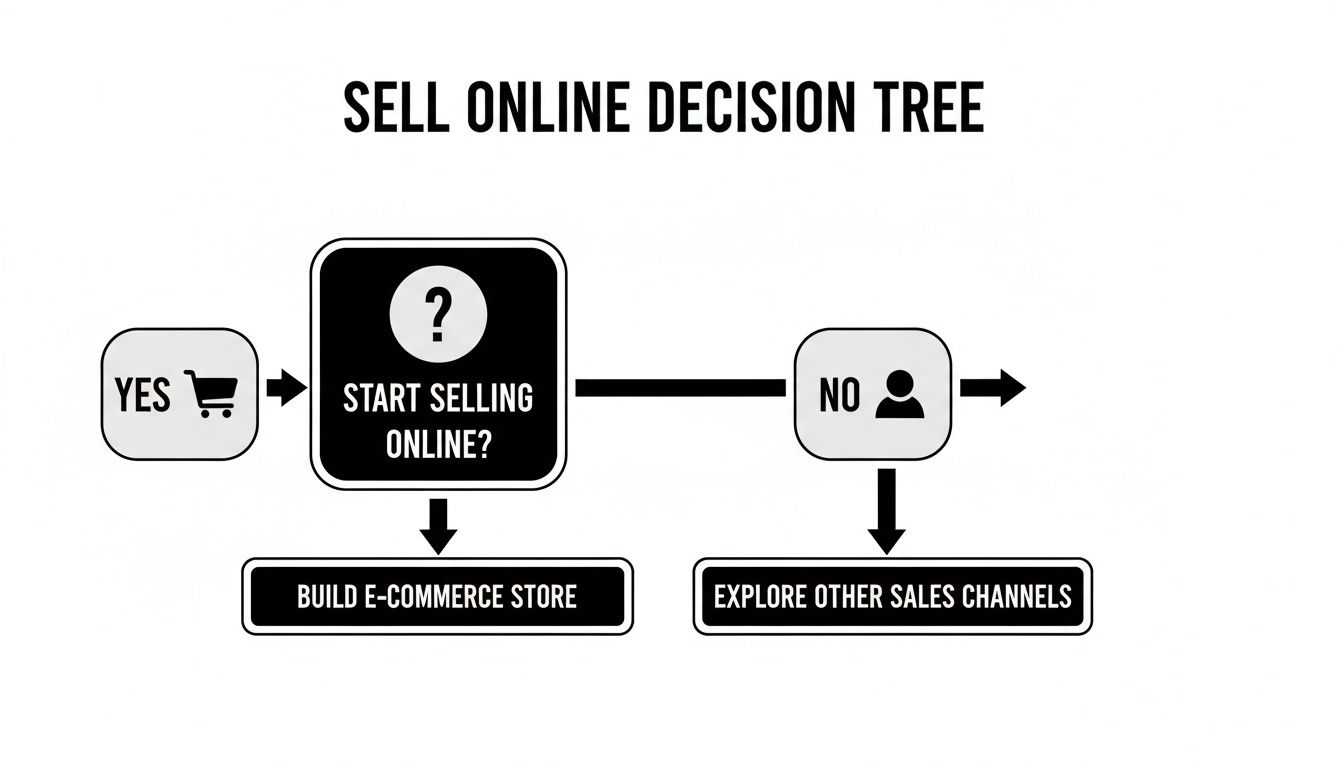

This decision tree gives you a good visual starting point. Are you building out a full e-commerce store, or are you just looking for a straightforward way to sell directly?

As you can see, whether or not you already have a website is a key factor that points you down a specific path.

To make this choice clearer, let's compare the three main options side-by-side.

Comparing Payment Acceptance Methods

MethodBest ForTechnical Skill RequiredImplementation SpeedShareable PaylinksFreelancers, consultants, one-off sales, and businesses without a website.None.Immediate.Embedded CheckoutMost online businesses with a website looking for a seamless, on-brand experience.Minimal (copy-paste).Fast (minutes to hours).API & WebhooksSaaS platforms, marketplaces, and businesses needing full control and custom logic.High (development team needed).Slower (days to weeks).

Each of these has its place. The key is to match the tool to the job you need it to do right now, while keeping an eye on where your business is headed.

Shareable Paylinks: The Simple and Fast Route

The absolute quickest way to start getting paid is with a shareable payment link. It's basically a secure, hosted webpage where your customer can pop in their card details. The best part? No coding required. This makes it a fantastic option for anyone who doesn't run a traditional e-commerce site.

Think of it as a supercharged digital invoice. You generate a unique link for a product or service and send it to your customer through email, a text message, or even a social media DM.

Who it's for: This is the go-to for freelancers, coaches, consultants, and creators selling digital goods.

Real-world scenario: Imagine a design agency in London wraps up a project for a client in New York. Instead of waiting on a slow, expensive international wire transfer, they just create a paylink for the final invoice. The client clicks, pays with their card, and the whole thing is settled in minutes.

Key benefit: You can be up and running almost instantly, without needing a website or any technical help.

For direct sales and invoicing, paylinks are a game-changer. They strip out all the friction and give you a professional way to collect a one-time payment or even kick off a simple subscription, which is often the simplest starting point for accepting credit cards for a small business.

Embedded Checkouts: A Seamless On-Site Experience

If you have your own website or app, an embedded checkout is probably your sweet spot. It lets you add a pre-built payment form directly onto your site, so the customer never has to leave. This is huge for building trust and can make a real difference in your conversion rates.

Because the checkout form itself is handled by your payment provider, you get that smooth, integrated feel without taking on the headache of managing sensitive card data yourself. All the heavy lifting for PCI compliance is offloaded.

What to Look for in an Embedded Checkout:

Brand consistency: You should be able to customize the colors, fonts, and layout to match your site perfectly.

Reduced friction: Keeping customers on your domain avoids that jarring redirect to another website—a classic spot where people abandon their carts.

Built-in security: Your payment provider is handling the complex security and compliance rules in the background.

This approach offers the ideal balance of control, security, and ease of use for most online businesses.

APIs And Webhooks: For Complete Customization

For businesses that need total control and deep integration, using an API (Application Programming Interface) is the way to go. This route allows your developers to build a completely custom payment flow from scratch, right inside your own platform.

An API lets you design unique subscription models, trigger all sorts of automated workflows, and sync payment data with your other business tools, like accounting software or a CRM. To make this work, webhooks are essential. They act as real-time notifications, pinging your application about events like successful payments or failed subscription renewals. When you're building at this level, truly understanding Credit Card Processing: How It Works is non-negotiable.

Who it's for: SaaS companies, online marketplaces, and any platform with complex billing rules or custom user journeys.

Real-world scenario: A subscription box company uses a payment API to manage its different monthly plans. As soon as a customer's payment goes through, a webhook automatically fires off an order to their fulfillment center. No manual work needed.

Key benefit: You get unparalleled flexibility to build a payment experience that does exactly what your business needs it to do.

Picking the right path from the start lays the foundation for how you’ll manage revenue, interact with customers, and ultimately, grow your business.

Getting Your Account Set Up and Staying Compliant

So, you've picked a method for taking payments. Awesome. The next part is actually opening an account with a payment provider and getting through the setup and compliance maze. It sounds like a headache, but honestly, modern platforms have made this part incredibly simple. They do most of the heavy lifting behind the scenes.

This whole process isn't just red tape—it's about building a secure foundation. When providers verify who you are, they're protecting everyone from fraud: you, your customers, and themselves.

What to Expect During Onboarding

When you sign up, you'll run into something called KYC and KYB, which stands for Know Your Customer and Know Your Business. This is standard practice across all financial services, so don't be alarmed.

You'll probably be asked for a few things:

Personal ID: A driver's license or passport to prove you are who you say you are.

Business Details: The official registered name of your company, its address, and any registration numbers.

Ownership Info: Who are the key people behind the business? They'll want to know.

This is all about confirming that you're a legitimate operation. It’s a crucial step in preventing financial crime and making sure the entire payment ecosystem stays trustworthy.

Let's Talk About PCI DSS Compliance (The Easy Way)

One term that scares a lot of new merchants is PCI DSS, or the Payment Card Industry Data Security Standard. It's basically a set of non-negotiable security rules for anyone handling credit card information, designed to keep that sensitive data safe.

Now, if you were to handle raw credit card numbers on your own servers, you’d have to go through a brutal and costly certification process. It's a massive distraction for most businesses.

The smartest way to deal with PCI compliance is to sidestep it entirely. Use a payment provider's hosted or embedded checkout, and they shoulder nearly all that responsibility for you.

These providers are built to be PCI-DSS Level 1 certified, which is the highest security certification you can get. They go through rigorous annual audits to prove their systems are secure, which means you don't have to. For a deeper dive, a good PCI DSS compliance checklist can be a lifesaver in making sure all your bases are covered.

Don't Forget These Key Security Layers: SCA and 2FA

Beyond PCI, there are a couple of other security measures that are absolutely essential, especially if you have international customers.

If you sell into Europe, you need to know about Strong Customer Authentication (SCA). It's a legal requirement over there that adds an extra verification step for online payments. Customers have to confirm their identity with two out of three possible methods:

Something they know (like a password)

Something they have (like their phone)

Something they are (like a fingerprint scan)

Picking a processor with SCA built right into their checkout is a must for selling to European customers. Without it, you’ll see a lot of failed payments. You can get a better sense of these requirements by looking into our approach to compliance.

Finally, lock down your own account. Two-Factor Authentication (2FA) is your best friend here. It adds a simple but powerful layer of security to prevent anyone from getting into your account and messing with your money. Always, always turn it on.

With U.S. credit card spending at $3.6 trillion and growing 5% each year, the opportunity is massive. For freelancers and agencies billing clients around the world, things like SCA and 2FA aren't just nice-to-haves—they're fundamental to doing business safely and successfully.

What's This Really Going to Cost Me?

Once you’ve jumped through the hoops of getting set up, the question on every business owner's mind is always the same: "What's the real cost of all this?" Let's be honest, the advertised price is almost never what you actually pay. Getting a handle on the fee structures is non-negotiable if you want to protect your profit margins, especially when your customers are all over the world.

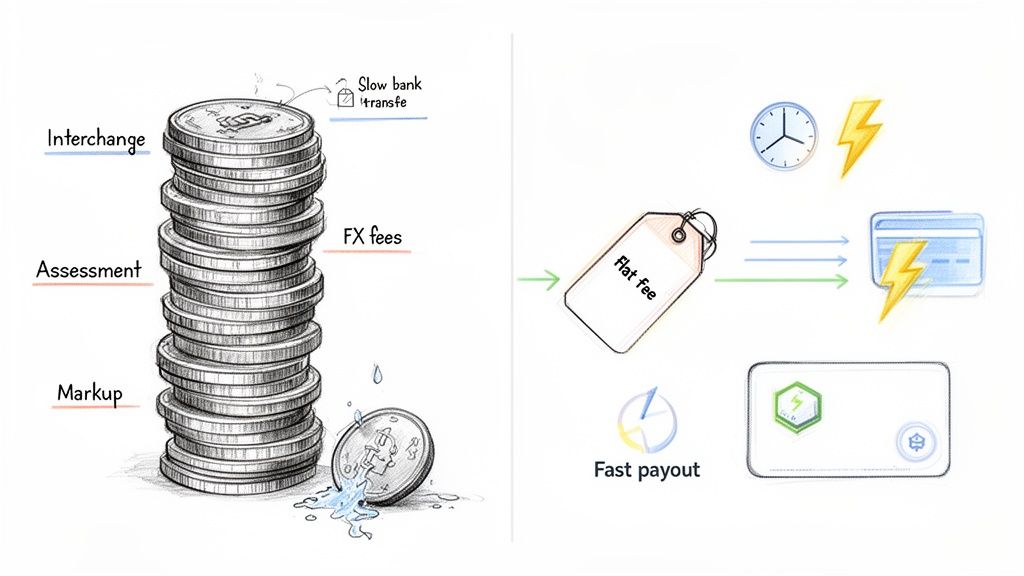

Traditional payment processors have a knack for building confusing, multi-layered fee structures. It feels a lot like those old cell phone bills where you'd see your plan's price and then a dozen little taxes and surcharges you never saw coming.

This picture really says it all. You've got the old, messy way that quietly eats at your revenue versus a clean, predictable approach. One creates uncertainty, the other gives you clarity.

The Old Way: A Mess of Hidden Fees

Many processors still use what’s called an "interchange-plus" model. This means that for every single transaction, you're getting hit with three separate charges:

Interchange Fee: This is the big one. It goes straight to the customer's bank (the issuing bank) and is set by the card networks like Visa and Mastercard. It’s non-negotiable.

Assessment Fee: A much smaller fee that goes directly to the card network itself.

Processor Markup: This is the only slice of the pie your payment processor actually keeps. It's their profit for handling the transaction.

While this setup can sometimes be cheaper for very high-volume, domestic-only businesses, it makes your costs wildly unpredictable. Even worse, it often conceals the single biggest expense for anyone selling internationally.

The Real Killer: Cross-Border Sales Costs

For merchants with a global customer base, the true profit-killer is almost always the foreign exchange (FX) conversion fee. When a customer in Japan pays you in yen for an item priced in dollars, a bank has to convert that currency.

This is where things get murky. Banks rarely give you the real-time market rate. Instead, they apply their own less-favorable rate and often tack on a conversion fee, which can easily skim an extra 1-3% off the top. This fee is usually buried deep in the fine print, silently eroding your revenue on every international sale. Our all-in pricing model was specifically designed to get rid of these nasty surprises.

The most expensive part of accepting international payments isn't the visible processing fee; it's the invisible currency conversion costs and slow settlement times that drain your profits and choke your cash flow.

A Better Way: Flat-Rate Pricing and Faster Money

Thankfully, the industry has started to move toward a much simpler, all-in-one pricing model. With this approach, you pay one flat percentage for every transaction. Period. It doesn't matter what kind of card it is or where your customer lives.

This gives you cost predictability. You know precisely what a $100 sale will cost you, whether the buyer is next door or on the other side of the planet. All those interchange, assessment, and other random fees are bundled into that one simple rate.

But the real game-changer isn't just about clearer fees—it's about how quickly you actually get your hands on your money.

Settlement: The Journey of Your Money

After a customer’s payment is approved, the money doesn’t just magically appear in your bank account. It has to go through a settlement process, which has historically been a slow, frustrating journey.

First, the funds land in your merchant account, where they might sit for a couple of days. Then, they begin another slow transfer to your actual business bank account via systems like ACH (in the U.S.) or SWIFT (for international wires), which is why many global sellers now look for a faster SWIFT alternative. All these steps add up. It’s not uncommon to wait three to seven business days—or even longer—to access your own revenue.

This delay creates a huge cash flow problem, especially for smaller businesses and freelancers who depend on that money to operate.

The USDC Payout Advantage

This is where a modern approach really shines. Instead of sending your money through the old, slow banking system, some platforms can deposit your revenue directly into a USDC wallet, which is a core reason to compare crypto payment processors for global business when you sell across borders.

USDC is a stablecoin, a type of cryptocurrency that's pegged 1:1 to the U.S. dollar. This offers a few massive advantages:

Speed: Payouts happen in minutes or hours, not days.

No Banking Friction: You completely bypass the legacy banking system. This means no more surprise payout holds, transfer limits, or frozen accounts—all common headaches for cross-border businesses.

Zero FX Fees: You settle in a dollar-equivalent asset, which completely eliminates forced currency conversions and all their hidden costs.

Credit cards are more dominant than ever, accounting for 35% of all US consumer transactions in 2024—a huge leap from just 18% nine years ago. As cards continue to fuel both online and in-person sales, how fast you get paid becomes a serious competitive edge. As these credit card trends from SellersCommerce show, models like USDC payouts are the answer, cutting through the delays and holds of traditional banking.

Handling Refunds And Customer Disputes

Taking a customer's payment isn't the end of the road—it’s just the beginning. No matter how great your product or service is, you're going to run into two inevitable post-sale scenarios: refunds and chargebacks. Knowing the crucial difference between them, and having a solid plan for each, is fundamental to protecting your revenue and your business's reputation.

Let's get the definitions straight. A refund is a simple, direct request from your customer for their money back. It’s a conversation between you and them. A chargeback, on the other hand, is a much more serious affair. This is a forced payment reversal kicked off by the customer’s bank, essentially a formal dispute where they claim the charge was fraudulent, the item never arrived, or the service wasn't what they paid for.

While both end with money going back to the customer, chargebacks are a different beast. They come with penalty fees from your processor and can seriously damage your standing with card networks like Visa and Mastercard. If your chargeback rate gets too high, you risk losing your merchant account entirely. That’s why your first line of defense is always making the refund process as painless as possible.

Making Refunds Easy (And Chargebacks Rare)

If a customer has a legitimate reason for a refund but can't figure out how to get one from you, their next phone call will be to their bank. And that's how chargebacks are born. A smooth, transparent refund process isn't just good customer service; it's your most effective tool for chargeback prevention.

Here’s what a solid refund workflow looks like in practice:

A Clear, Findable Policy: Your refund policy needs to be easy to find on your website. Write it in simple, human language, and clearly outline the terms (e.g., within 30 days, item must be unopened).

A Simple Way to Start: Let customers request a refund through a straightforward contact form, a dedicated email address, or a button right in their account dashboard. Don't make them solve a riddle just to ask for their money back.

Speedy Processing: Once you’ve approved the refund, act on it. Modern payment platforms usually let you issue full or partial refunds with just a click, right from the transaction details.

A pro tip from my experience: look for a payment provider that offers zero-fee refunds. Some platforms not only give the customer their money back but will also credit you for the original processing fee. This little detail can save you a surprising amount of money on returned sales.

This kind of proactive approach shows customers you’re confident in what you sell and you value their business. It can turn a potentially negative experience into a neutral, or even positive, one.

Responding To Chargebacks When They Happen

Even with the best refund policy, chargebacks will occasionally slip through. When you get that notification, the clock starts ticking. You typically have a window of 15 to 45 days to respond with evidence proving the transaction was legitimate. Ignoring a chargeback is an automatic loss—you lose the sale amount and get slapped with a penalty fee.

To win a dispute, you need to arm yourself with compelling evidence. The exact documents depend on the reason for the chargeback (e.g., "fraud" versus "product not received"), but your goal is to build an undeniable case.

Here’s the kind of evidence you should gather:

Proof of Purchase: Think invoices, digital receipts, or order confirmations that clearly connect the customer to the purchase.

Communication History: Any emails, support tickets, or chat logs are incredibly valuable, especially if the customer acknowledged receiving the product or service.

Delivery Confirmation: This is a big one. For physical goods, provide shipping receipts and tracking numbers showing a successful delivery. For digital products, server logs showing a download or account login can work.

Policy Agreement: Show proof that the customer had to check a box or otherwise agree to your terms of service and refund policy during checkout.

Your payment provider’s dashboard is your command center for this whole process. It's where you'll get the dispute notification, see the reason code from the bank, and upload your evidence. Staying organized and responding quickly with clear, well-documented proof is your best shot at winning the dispute and getting your money back.

Frequently Asked Questions About Accepting Card Payments

Getting into payment processing can feel like you're learning a new language. You've got questions, and you need straight answers from someone who's been there. Let's tackle some of the most common things merchants ask when they're figuring out how to accept card payments.

What’s the Cheapest Way to Accept Credit Card Payments?

This is the big one, but "cheapest" is tricky. The advertised rate you see from a processor is rarely the full story, especially if you have customers all over the world.

That rock-bottom percentage often conveniently leaves out a bunch of other costs that creep up on you. You've got interchange and assessment fees that go to the card networks, monthly account fees, and a dozen other little charges. But the real killer for international businesses is the foreign exchange (FX) fee, which can quietly skim an extra 1-3% off every single sale.

For most businesses selling globally, a simple flat-rate model is usually much more transparent and cost-effective. You get one predictable number, and all those other sneaky fees are already baked in. The best-case scenario? Find a provider that eliminates FX fees entirely by settling your revenue in a stablecoin like USDC, and it is worth reviewing the top crypto payment processors for merchants in 2026 to see which ones support that model. This move alone can drastically cut your real processing costs by getting rid of the single biggest hidden expense of cross-border sales.

The cheapest way to accept card payments isn't about chasing the lowest advertised rate. It's about finding an all-in pricing model that eliminates expensive surprises, especially currency conversion fees.

Do I Need a Business Bank Account to Accept Payments?

It used to be a hard "yes." For decades, the only way to get your money was through a traditional business bank account. Processors would send your funds through slow, clunky systems like SWIFT or ACH, and you just had to wait.

Thankfully, things have changed. Modern payment platforms give you another option: settling your funds directly to a USDC wallet.

This isn't just a novelty; it offers real advantages. Your payouts arrive in minutes or hours, not days. It also lets you sidestep the common frustrations of traditional banking, like sudden payout holds, arbitrary transfer limits, or even frozen accounts—all of which are massive headaches for global businesses. For digital creators or international companies, holding funds in a stablecoin offers speed and flexibility that old-school banks just can't match.

How Long Does It Take to Get Started?

You can get up and running surprisingly fast—often in just a few minutes. The days of faxing paperwork and waiting weeks for approval are long gone. Most of the process is now completely automated.

The main step is getting your identity and business verified, which you'll hear called KYC (Know Your Customer) and KYB (Know Your Business). Even that is usually sorted out the same day you sign up.

Once you’re verified, you can go live almost immediately. If you use pre-built tools like shareable payment links or an embeddable checkout, you can start selling right away with zero coding. And for those who need a more custom setup with an API, the account approval is just as quick. The only thing that takes time is your own development work.

What Is PCI Compliance and Should I Worry About It?

PCI DSS (Payment Card Industry Data Security Standard) is a set of mandatory security rules created to keep cardholder data safe from fraudsters. If you were to handle and store raw credit card numbers on your own servers, you'd be on the hook for a complex, expensive, and never-ending compliance process.

The good news is you shouldn't have to worry about it.

When you work with a modern payment provider, you're offloading almost all of that responsibility. They invest huge amounts of time and money to become PCI-DSS Level 1 certified—the highest security standard there is. By using their hosted or embedded checkout tools, you ensure that sensitive card data never even touches your servers. They handle the secure capture, transmission, and storage, so you don't have to. It's the smartest and safest way to deal with compliance, freeing you up to focus on growing your business.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, while you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. That means you can accept credit card payments globally, go live in minutes with paylinks, an embedded checkout, or an API, and skip the FX fees, payout holds, and PCI headaches of the old way. Start selling worldwide today.